Major stock indices declined in the first part of the week as many jittery investors remain concerned over AI-related company valuations. Then, a flood of economic data triggered a rally at the end of the week, sending some indices back above their all-time highs.

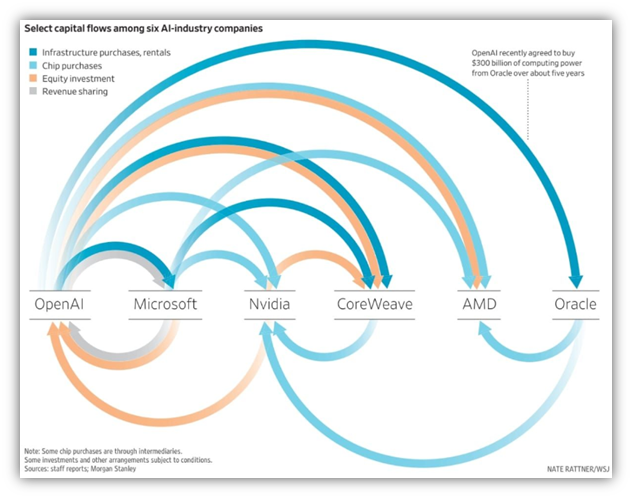

The question regarding AI company valuations is a legitimate one. One concern is the question, have we gone too far too fast with AI company stock prices? Another concern is the increasing number of “circular” deals between many of these companies that could be clouding their actual financial performance.

Essentially, Company A buys a product or invests in Company B, and Company B uses that money to buy product or invest in Company A.

Some analysts are sounding the alarm that this is similar to the flurry of shaky vendor financing deals done during the Tech Bubble. However, while there are some similarities, there are many differences as well.

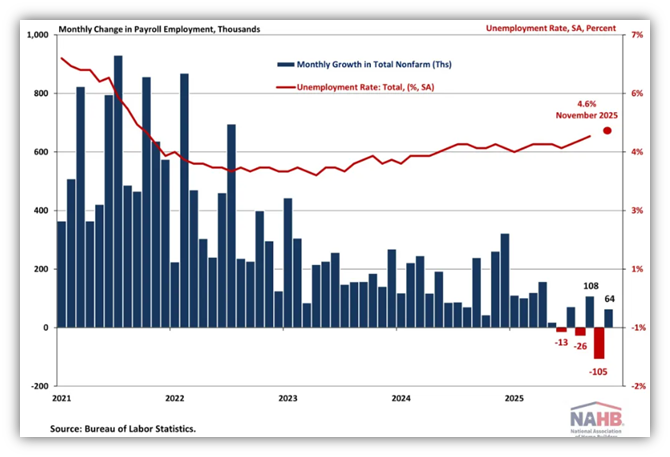

We had two big economic data releases this week – jobs and inflation. This data dump comes as the US government is working to catch up from reporting delays due to the government shutdown. The US economy created 64,000 jobs in November vs the Dow Jones estimate of 45,000, but the jobs reports shows it was more complicated than that. According to the data, October showed 105,000 job losses and the unemployment rate rise from 4.4% to 4.6%.

The graph clearly shows the labor market sputtering in the last half of this year. But according to Brian Wesbury, Chief Economist at First Trust Advisors,

“…it’s important to recognize that given the huge policy shift from lax to strict immigration enforcement, the push by the Trump Administration to thin government payrolls, as well as the ongoing aging of the population and layoffs attributed to AI, payroll growth should be slow.”

https://www.ftportfolios.com/Blogs/EconBlog/2025/12/15/no-more-flying-blind

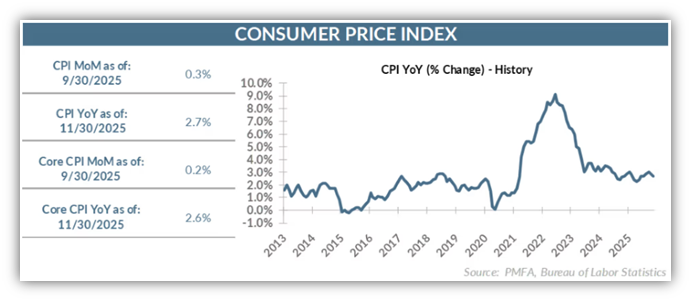

Then, on Thursday we received the inflation report that showed inflation slowing to 2.7% vs an expected rise to 3.1%.

This may be good news if the data is correct, and that’s the big concern for both the jobs data and the inflation data we received this week. There are many reasons to be skeptical about the details of both reports given how the government shutdown has affected the collection of the data and the data itself. That’s why the December report will be of heightened interest when it’s released next month as it is expected to represent a “normal” month of reporting.

Have a very merry Christmas and a happy New Year.

Jack C. Harmon II, CFP®, CIMA

Principal, Harmon Financial Advisors

Registered Principal, Raymond James Financial Services

Harmon Financial Advisors, Inc. is an independent, fee-based financial planning firm and an independent Registered Investment Advisor. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. and Harmon Financial Advisors, Inc. Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC. Harmon Financial Advisors, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services, Inc.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information in this commercial email has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Harmon Financial Advisors, Inc. and not necessarily those of RJFS or Raymond James.

There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results.

Investing involves risk and you may incur a profit or loss regardless of strategy selected. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary.

Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. There is an inverse relationship between interest rate movements and fixed income prices. Generally, when interest rates rise, fixed income prices fall and when interest rates fall, fixed income prices rise.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Investments & Wealth Institute™ (The Institute) is the owner of the certification marks “CIMA” and “Certified Investment Management Analyst.” Use of CIMA and/or Certified Investment Management Analyst signifies that the user has successfully completed The Institute’s initial and ongoing credentialing requirements for investment management professionals.