Markets continue to rise and fall on speculation related to the conflict in Iran. While it’s certainly possible that some sort of resolution could come in the next week or two, we believe the markets have been too optimistic and likely remain so. Markets have so far taken President Trump at his word – this is a 4- to 6-week affair. We’re roughly 4 weeks into this conflict, so that makes developments over the next two weeks, or lack thereof, very important for markets.

Extra oil supplies have been added to global markets to blunt the shock of losing 20% of global oil supply through the Strait of Hormuz. 32 Member countries of the International Energy Agency unanimously agreed to make 400 million barrels of oil from their emergency reserves available to the market earlier this month. As of February 2026, approximately 300 million barrels of Russian and Iranian oil were at sea, stored in a “shadow fleet” of tankers attempting to skirt US sanctions on its sale. The US has temporarily suspended sanctions on this oil, allowing it to enter the market. This 700-million-barrel injection of oil has, so far, kept oil prices from spiking even higher, but this additional oil supply will be gone in the next 2 weeks.

https://mei.edu/policymemo/how-iran-china-and-russia-use-the-shadow-fleet-to-evade-us-sanctions/

Without additional supply, energy prices will likely move even higher over the coming weeks.

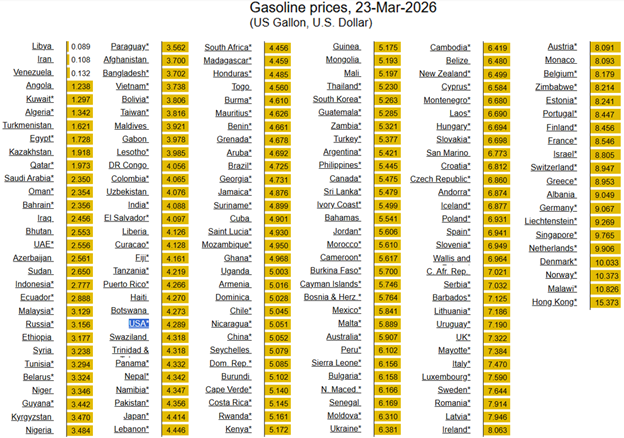

Here’s what other countries are currently paying for gasoline, with the cheapest on the left and more expensive as you move right across the table. USA is highlighted in blue.

https://www.globalpetrolprices.com/gasoline_prices/

This type of uncertainty reminds us why diversification and flexibility in portfolio design are so important. While major stock indices are lower for the year and bond indices are relatively flat, many alternative investment strategies remain positive. Alternative investment strategies are designed with the intention of generating positive returns over time while not depending heavily on positive returns in the stock or bond markets.

Additionally, our proprietary tactical risk model has become increasingly conservative during March, remaining positive year-to-date and is positive today (as of noon).

I probably won’t write an email next week as I will be on vacation in the North Georgia mountains with family coming to visit from Ohio.

Have a great weekend.

Jack C. Harmon II, CFP®, CIMA

Principal, Harmon Financial Advisors

Registered Principal, Raymond James Financial Services

Harmon Financial Advisors, Inc. is an independent, fee-based financial planning firm and an independent Registered Investment Advisor. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. and Harmon Financial Advisors, Inc. Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC. Harmon Financial Advisors, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services, Inc.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information in this commercial email has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Harmon Financial Advisors, Inc. and not necessarily those of RJFS or Raymond James.

There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results.

Investing involves risk and you may incur a profit or loss regardless of strategy selected. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary.

The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stocks of companies maintained and reviewed by the editors of the Wall Street Journal.

The Dow Jones Corporate Bond Index is an equally weighted basket of 96 recently issued investment-grade corporate bonds with laddered maturities. The index intends to measure the return of readily tradable, high-grade U.S. corporate bonds. It is priced daily.

The MSCI ACWI ex USA Index captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 24 Emerging Markets (EM) countries. With 1,983 constituents, the index covers approximately 85% of the global equity opportunity set outside the US.

Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. There is an inverse relationship between interest rate movements and fixed income prices. Generally, when interest rates rise, fixed income prices fall and when interest rates fall, fixed income prices rise.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Investments & Wealth Institute™ (The Institute) is the owner of the certification marks “CIMA” and “Certified Investment Management Analyst.” Use of CIMA and/or Certified Investment Management Analyst signifies that the user has successfully completed The Institute’s initial and ongoing credentialing requirements for investment management professionals.