There have been a lot of investor discussions around a couple of paradoxes lately that deserve some attention.

First of all, stocks continue to hover near all-time highs in spite of the stalemate in the Middle East. This has caused confusion for many investors who believe the markets have it all wrong. The markets are too optimistic and the geopolitical risk isn’t reflected in the prices of stocks they say. And they may be right.

But there are other things going on in the world that affect the markets, and some of them don’t get as much coverage in the mainstream media as the war. For example, we’re currently in earnings season and we’re learning that US corporations have been doing much better than expected so far this year. Of the 70 companies in the S&P 500 that have reported 1st quarter earnings so far, 89% have beaten their consensus estimates. In aggregate, corporate earnings are running about 10% above expectations. While some optimistic investors buying, many are simply hesitant to sell stocks in this good earnings environment.

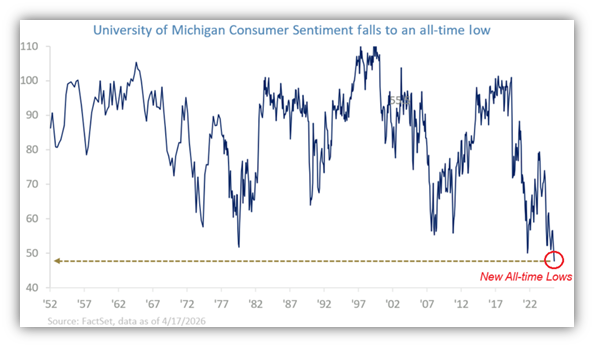

There’s another potential disconnect that has come to light this week regarding the markets and the economy. The University of Michigan Consumer Sentiment Index fell to a record low of 47.6 in early April, the lowest reading in the 70-plus-year history of the survey.

Are things really that bad? And how can the stock market be at all-time highs if people believe the economy is worse than it was in the 1970s? Nobel Prize-winning economist Paul Krugman had this to say about the sentiment survey –

“Obviously, I’m no defender either of Trump’s policies or of his lies. But while the US economy isn’t nearly as good as he claims, it’s objectively not bad enough to justify the worst consumer sentiment in history — worse than during the stagflation at the end of the 1970s, worse than in the aftermath of the 2008 financial crisis.”

https://paulkrugman.substack.com/p/lies-damned-lies-and-economic-vibes

The leading hypothesis among many economists is that it’s all about prices. First of all, consumers easily remember the lower prices and the long period of slow inflation prior to Covid as it was just a few years ago. Additionally, consumers have been promised by politicians that their policies would bring lower prices, which they could not and did not. Many consumers don’t understand that a lower inflation rate does not mean lower prices, resulting in frustration and disappointment. And now with the prospect of accelerating inflation driven by higher energy prices, consumers are in a funk.

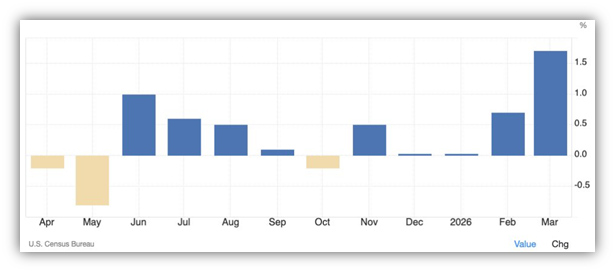

While consumers may feel bad about the economy, they thankfully haven’t slowed their spending yet. After rising 0.7% in February, US retail sales jumped 1.7% in March.

Unfortunately, most of the spike in spending was attributed to gasoline, but even when gas station sales are excluded, retail sales still rose a healthy 0.6% in March.

Have a great weekend.

Jack C. Harmon II, CFP®, CIMA

Principal, Harmon Financial Advisors

Registered Principal, Raymond James Financial Services

Harmon Financial Advisors, Inc. is an independent, fee-based financial planning firm and an independent Registered Investment Advisor. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. and Harmon Financial Advisors, Inc. Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC. Harmon Financial Advisors, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services, Inc.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information in this commercial email has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Harmon Financial Advisors, Inc. and not necessarily those of RJFS or Raymond James.

There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results.

Investing involves risk and you may incur a profit or loss regardless of strategy selected. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Investments & Wealth Institute™ (The Institute) is the owner of the certification marks “CIMA” and “Certified Investment Management Analyst.” Use of CIMA and/or Certified Investment Management Analyst signifies that the user has successfully completed The Institute’s initial and ongoing credentialing requirements for investment management professionals.