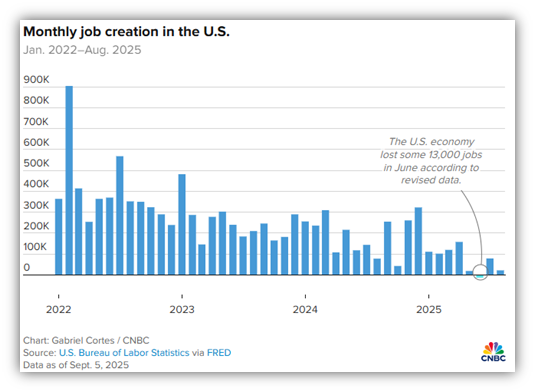

The markets received some key data Friday morning as the August jobs report was released. It showed that the US economy created fewer jobs than expected – just 22,000 versus a forecast of 75,000. This is a continuation of a long trend of a weakening, but not weak, labor market.

https://www.cnbc.com/2025/09/05/jobs-report-august-2025.html

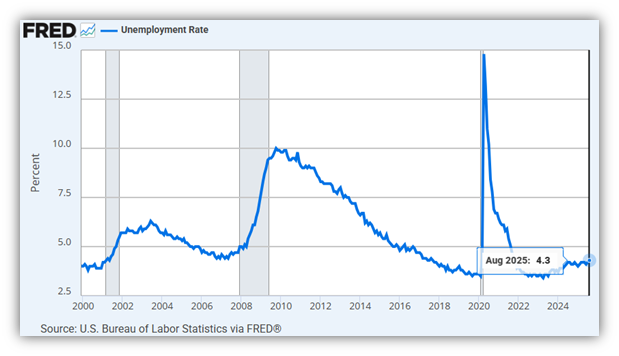

I say the US labor market is not weak because the unemployment rate rose last month to just 4.3% from 4.2% in July. The labor force participation rate edged higher to 62.3% and the labor force swelled by 436,000, accounting for the tick higher in the unemployment rate as more people began looking for jobs.

The unemployment rate rose to 4.2% in July 2024 and has hovered around this level for over a year now. For comparison, here are some unemployment rates from around the world.

Australia 4.21%

Brazil 6.10%

Canada 6.32%

China 5.10%

Denmark 4.89%

EUROPEAN UNION 6.00%

France 7.36%

Germany 3.29%

Greece 9.36%

India 5.10%

Ireland 4.38%

Italy 5.80%

Japan 2.50%

Mexico 2.80%

Norway 3.80%

Poland 2.93%

Russia 3.12%

South Africa 33.20%

South Korea 3.00%

Spain 10.29%

Sweden 8.36%

Switzerland 2.25%

Turkey 8.50%

United Kingdom 4.15%

https://en.wikipedia.org/wiki/List_of_countries_by_unemployment_rate

This disappointing jobs report has dramatically increased the odds for interest rate cuts through the remainder of the year. The markets are now pricing in a 100% chance of a rate cut the next time the Fed meets this month.

September 17th meeting 100% chance of an interest rate cut

October 29th meeting 81% chance of a second interest rate cut

December 10th meeting 77% chance of a third interest rate cut

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

So, it’s the Fed to the rescue – maybe. We’ll have to see if lower borrowing costs will be enough to clear the cloud of uncertainty keeping companies from hiring more employees. There’s a lot of uncertainty out there and while the markets will welcome lower rates, I’m not sure if it will be enough for companies to overcome concerns over tariffs, inflation, immigration, and global tensions. I hope so.

I’ll be traveling next week so there may or may not be a weekly email. Just more uncertainty.

Have a great weekend.

Jack C. Harmon II, CFP®, CIMA

Principal, Harmon Financial Advisors

Registered Principal, Raymond James Financial Services

Harmon Financial Advisors, Inc. is an independent, fee-based financial planning firm and an independent Registered Investment Advisor. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. and Harmon Financial Advisors, Inc. Securities offered through Raymond James Financial Services, Inc. Member FINRA/SIPC. Harmon Financial Advisors, Inc. is not a registered broker/dealer and is independent of Raymond James Financial Services, Inc.

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information in this commercial email has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Harmon Financial Advisors, Inc. and not necessarily those of RJFS or Raymond James.

There is no guarantee that these statements, opinions, or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results.

Investing involves risk and you may incur a profit or loss regardless of strategy selected. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor’s results will vary.

Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. There is an inverse relationship between interest rate movements and fixed income prices. Generally, when interest rates rise, fixed income prices fall and when interest rates fall, fixed income prices rise.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®, and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Investments & Wealth Institute™ (The Institute) is the owner of the certification marks “CIMA” and “Certified Investment Management Analyst.” Use of CIMA and/or Certified Investment Management Analyst signifies that the user has successfully completed The Institute’s initial and ongoing credentialing requirements for investment management professionals.